The decision to secure international travel insurance is no longer a mere suggestion but a critical component of responsible global mobility, shielding travelers from potentially ruinous financial burdens in the event of unforeseen incidents. While the prospect of selecting a policy can appear daunting due to complex terminologies and varied offerings, understanding the fundamental necessity and key features is paramount. This guide aims to demystify the landscape of international travel insurance, providing a comprehensive overview of its value, common coverage types, factors influencing policy choice, and insights into leading market providers.

The Indispensable Value of International Travel Insurance

The question of whether international travel insurance is a worthwhile investment is unequivocally answered in the affirmative. Historically, some travelers opted to forego insurance, particularly in regions perceived to have lower medical costs. However, this approach critically overlooks the potential for severe accidents or illnesses that necessitate specialized care or emergency medical evacuation, which can incur costs skyrocketing into the tens or even hundreds of thousands of dollars. For instance, an air ambulance evacuation from a remote location in South America to a major medical facility can easily exceed $50,000, while a serious hospital stay in a country with high medical expenses, such as the United States, can quickly accumulate bills surpassing $100,000. These figures underscore the profound financial risk assumed by uninsured travelers.

Beyond individual financial protection, the global travel landscape increasingly mandates insurance. Countries like Cuba, Qatar, and Ecuador explicitly require proof of travel insurance for entry, a trend that reflects a broader international effort to ensure visitors can cover potential medical costs and avoid burdening local healthcare systems. This regulatory shift highlights the recognition of travel insurance not just as a personal safeguard, but as an integral part of international health and safety protocols. Furthermore, a robust policy extends its utility beyond medical emergencies, offering protection against a spectrum of risks, including accidental death benefits, crisis response in politically unstable regions, and assistance during natural disasters, thereby offering comprehensive peace of mind that trivial daily expenses cannot replicate. With many comprehensive policies averaging a cost of $2 to $4 per day, the expenditure is a negligible fraction of overall travel budgets, making the decision to opt out a significant, and often ill-advised, gamble.

Comprehensive Coverage: What to Expect from a Policy

Understanding the scope of international travel insurance is crucial, as policies vary significantly in their offerings and exclusions. Diligent review of the fine print is always advised, but generally, a comprehensive policy should address a wide array of potential travel disruptions and emergencies.

Core Medical and Emergency Benefits:

- Emergency Medical Expenses: Coverage for hospital stays, doctor’s visits, surgeries, prescription medications, and other medical treatments incurred due to unforeseen illness or injury abroad. Policy limits typically range from $50,000 to several million dollars.

- Emergency Medical Evacuation: Crucial for travelers in remote areas, this covers the cost of transporting an injured or ill individual to the nearest appropriate medical facility, which could involve air ambulances or specialized ground transport.

- Repatriation of Remains: In the tragic event of a traveler’s death abroad, this covers the costs associated with preparing and transporting the remains back to their home country.

- Emergency Dental Treatment: Coverage for sudden and acute dental pain requiring immediate attention.

- Accidental Death & Dismemberment: Provides a lump sum payment to beneficiaries in the event of accidental death or significant permanent injury.

- Crisis Response/Political Evacuation: Assistance and coverage for evacuation from a country due to political unrest, civil disturbance, or natural disaster, ensuring traveler safety.

Non-Medical Travel Protections:

- Trip Cancellation: Reimbursement for non-refundable expenses if a trip is cancelled due to covered reasons (e.g., sudden illness, severe weather, natural disaster at destination, job loss, death of a family member).

- Trip Interruption: Coverage for additional transportation costs and lost pre-paid expenses if a trip is cut short due to covered reasons.

- Lost, Stolen, or Delayed Baggage: Compensation for essential items if luggage is delayed, and reimbursement for the value of lost or stolen belongings. Specific limits and depreciation rules often apply.

- Travel Delay: Reimbursement for accommodation and meal expenses incurred due to significant flight or travel delays.

- Personal Liability: Coverage for legal costs and compensation if the traveler accidentally causes injury to another person or damages their property while abroad.

- Rental Car Damage: Coverage for damage to a rental vehicle (often an optional add-on).

Beyond these general categories, some advanced policies may include benefits for adventure activities, pre-existing medical conditions (with specific stipulations), and even non-medical services like emergency concierge support. For example, some insurers now offer coverage for mental health support and telemedicine consultations, reflecting evolving traveler needs. The critical takeaway remains that travelers must align their chosen policy’s coverage with their planned activities and potential risks.

Tailoring Insurance to Your Travel Profile

The "right" travel insurance policy is not universal; it is highly individualized, depending on a multitude of factors related to the traveler’s profile, destination, and planned activities. Prospective buyers must consider several key elements to ensure adequate protection.

Traveler Demographics and Itinerary:

- Age: Insurance premiums typically increase with age, reflecting higher health risks. Some policies may have age limits for eligibility, particularly for certain types of coverage or activities.

- Place of Residence: Eligibility for specific policies often depends on the traveler’s country of permanent residence. For expatriates or digital nomads who no longer maintain residency and healthcare in their home country, specialized long-term plans are crucial.

- Destination: Travel to countries with high medical costs (e.g., USA) or regions with known political instability or natural disaster risks may necessitate higher coverage limits or specific riders.

- Trip Length: Short-term leisure trips differ significantly from extended backpacking adventures or long-term digital nomad stays, each requiring different policy structures (e.g., single-trip vs. annual multi-trip vs. long-term medical).

Adventure and Activity Coverage:

A common pitfall for adventurous travelers is assuming standard policies cover all activities. Many extreme sports or high-risk activities – such as scuba diving beyond a certain depth, mountaineering above a specific altitude, heli-skiing, or even motorbiking/scooter riding – are often excluded from basic policies. Travelers planning such activities must explicitly seek policies or add-on riders that cover these specific risks. For instance, a policy covering motorbiking might require the traveler to hold a valid license for that vehicle type in their home country.

Pre-existing Medical Conditions:

Travelers with pre-existing medical conditions face particular challenges. Many standard policies exclude coverage for conditions that existed prior to purchasing the insurance. However, specialized policies or waivers can be obtained, often at a higher premium, provided the conditions are declared and meet specific criteria (e.g., stable for a certain period before travel). Failure to disclose pre-existing conditions can lead to claims being denied.

Deductibles and Policy Limits:

The deductible (the amount the insured must pay out-of-pocket before the insurance company pays) and the overall policy limits (the maximum amount the insurer will pay) directly impact premiums and the traveler’s financial exposure. Policies with lower deductibles or higher limits typically come at a higher cost. Travelers should balance these factors against their risk tolerance and budget.

Home Country Coverage for Expats:

A crucial, yet often overlooked, detail for digital nomads and long-term expatriates is coverage when returning to their home country for visits. Many expat insurance plans explicitly exclude coverage during periods spent in the country of origin, assuming local healthcare systems will apply. Travelers must verify this clause to avoid being uninsured during what might seem like a "safe" period.

Acquiring and Scrutinizing Your Policy

The process of purchasing international travel insurance has become streamlined, with most providers offering online quotes and immediate policy issuance. However, the convenience should not detract from the necessity of thorough due diligence.

The Purchase Process:

Travelers can obtain quotes directly from insurance providers’ websites or through comparison sites that aggregate offers from multiple insurers. Once a suitable policy is identified, the traveler provides personal and trip details, makes payment, and typically receives the policy documents via email within minutes or hours. Many companies offer a "free look" period (e.g., 10-14 days) during which the policy can be reviewed and canceled for a full refund if it doesn’t meet expectations, provided travel has not commenced. Flexibility is also a key consideration; some policies allow for extensions while abroad, which is invaluable for long-term travelers, while others require the traveler to return home to purchase a new policy.

Critical Questions to Ask Before Committing:

Engaging directly with insurance providers’ support staff is highly recommended to clarify any ambiguities in the policy wording. A comprehensive list of inquiries should include:

- Home Country Coverage: Does this policy provide any coverage when I visit my country of permanent residence, and if so, for what duration and under what conditions?

- Emergency Evacuation Scope: In a severe medical emergency (e.g., a broken back in a remote region), will the policy cover the entire cost of airlifting me to the nearest appropriate medical facility, or even repatriate me to my home country for ongoing care, rather than just the closest, potentially under-equipped, hospital?

- Medical Provider Network: Am I restricted to a specific network of hospitals or doctors, or can I seek treatment from any licensed medical professional? What is the process for direct billing versus reimbursement?

- Activity Exclusions: Does this policy cover all the adventure activities I plan to undertake (e.g., scuba diving, trekking at high altitudes, motorbiking)? Are there any specific conditions (e.g., licensing requirements for motorbiking) or blanket exclusions?

- Pre-existing Conditions: How are pre-existing medical conditions handled? What documentation is required, and are there waiting periods or specific exclusions?

- Insurer Solvency: What assurances are there regarding the company’s financial stability and ability to pay claims, particularly for long-term policies?

- Deductible Application: Is the deductible applied per claim, per incident, or per trip?

- Policy Extensions: Can I extend my policy while I am already traveling, or must I return home to re-insure?

- Pandemic/Epidemic Coverage: How does the policy respond to global health crises, such as pandemics? Are there specific exclusions related to travel advisories or government mandates?

These questions empower travelers to make an informed decision, ensuring their policy aligns perfectly with their travel plans and risk profile.

Leading Providers in the International Travel Insurance Market

The international travel insurance market features several prominent providers, each catering to specific segments of the traveling population. While individual policy details are paramount, a general understanding of their market positioning can guide initial research.

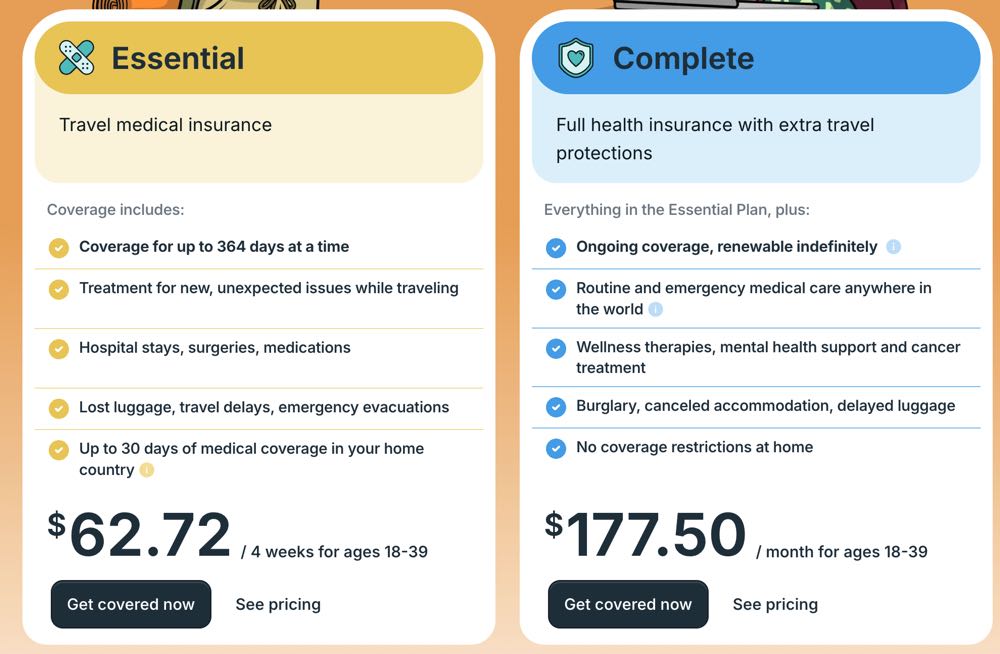

1. SafetyWing:

SafetyWing is a notable provider specializing in plans for digital nomads, remote workers, and long-term travelers. Its "Nomad Insurance" is designed for individuals living and working abroad who may not have traditional home country health insurance.

- Strengths: Often lauded for its affordability, particularly for younger travelers (18-39), and its flexible, subscription-based model. It includes limited home country coverage (30 days per 90 days of coverage) and covers a range of adventure activities.

- Considerations: While comprehensive for its target demographic, it may have lower maximum coverage limits compared to traditional policies and specific exclusions (e.g., certain extreme sports, pre-existing conditions).

2. World Nomads Travel Insurance:

Widely recognized and often recommended by travel guidebooks, World Nomads targets backpackers and adventure seekers.

- Strengths: Renowned for covering a vast array of adventure activities (often including those deemed high-risk) and offering flexibility for purchasing and extending policies while already abroad. Their plans are generally comprehensive for short to medium-term adventurous trips.

- Considerations: Premiums can be higher, especially for older travelers or those seeking the most extensive coverage. Specific exclusions or higher deductibles may apply to certain activities.

3. Allianz International Travel Insurance:

A global leader in insurance, Allianz offers a broad spectrum of travel and expatriate insurance plans known for their reliability and extensive coverage options.

- Strengths: Offers various plans from single-trip to annual multi-trip and specialized expat health insurance, providing robust coverage limits and a reputable claims process. Their brand recognition often instills confidence.

- Considerations: Premiums can be on the higher end, especially for comprehensive plans. Expat plans may have specific limitations regarding home country visits, and adventure activity coverage might require specific add-ons or higher-tier plans.

4. True Traveller:

Primarily serving residents of the UK and Europe, True Traveller is a favored choice among backpackers and adventure enthusiasts from these regions.

- Strengths: Offers comprehensive coverage for a wide range of adventure sports and activities, tailored specifically for European travelers on extended trips. Known for its clear policy wording and responsive customer service.

- Considerations: Eligibility is restricted to residents of the UK and certain European countries. Like other adventure-focused insurers, specific exclusions or requirements for certain activities may apply.

5. Insurance Hotline (for Canadian residents):

For Canadian citizens, Insurance Hotline serves as a valuable comparison platform, allowing travelers to compare quotes from multiple Canadian insurance providers to find competitive rates for medical and trip coverage.

- Strengths: Facilitates significant savings by comparing various policies, offering a convenient way to access a wide range of options tailored to Canadian residents’ needs. Covers standard benefits like emergency medical, trip cancellation, and lost baggage.

- Considerations: As a comparison site, the actual policy terms and conditions are dictated by the underlying insurers. Travelers must still meticulously review the chosen policy’s fine print.

Traveling with Assured Peace of Mind

In an era of increasing global interconnectedness and unforeseen events, international travel insurance has evolved from a discretionary purchase to an indispensable element of travel planning. The complexities of global health systems, the potential for exorbitant medical costs, and the myriad of non-medical travel disruptions underscore the financial and logistical imperative of securing adequate coverage. By diligently researching policies, understanding their nuances, and asking pertinent questions, travelers can select a plan that aligns with their individual needs, destination, and activities. This proactive approach ensures that, regardless of the unexpected turns a journey may take, travelers can navigate the world with the profound assurance that they are protected, allowing for a truly peaceful and enriching experience.

{kind=link}