The Essential Framework of Modern Travel Insurance

Travel insurance is a multifaceted financial product designed to mitigate the risks associated with domestic and international movement. For the solo traveler, the primary focus is often twofold: emergency medical coverage and emergency evacuation. Unlike group travelers who may have a support network on the ground, a solo traveler who falls ill or suffers an injury—such as a fracture on a cobblestone street or a sudden illness in a remote region—must rely on the professional assistance services provided by their insurance carrier.

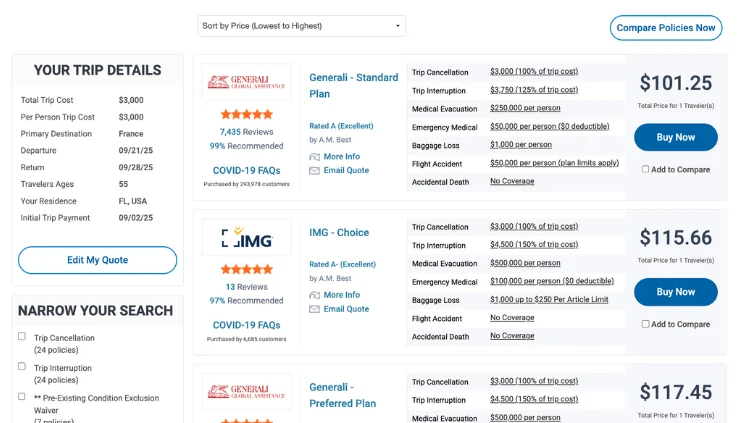

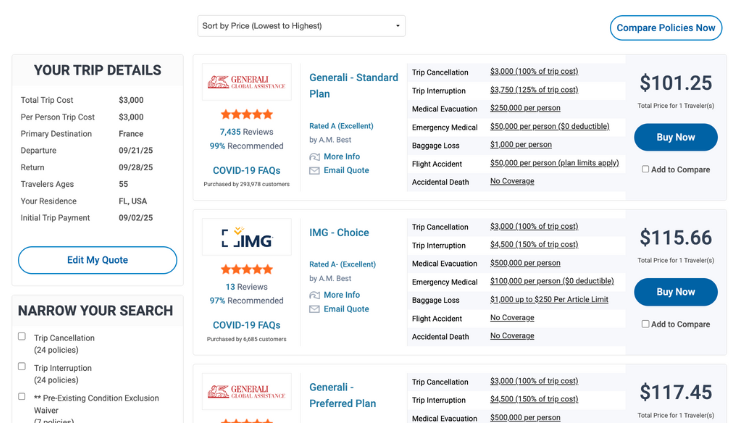

Medical emergencies are statistically more likely to occur when individuals are removed from their daily routines. Changes in diet, activity levels, and environment can trigger underlying conditions or lead to accidents. Professional medical observers note that travelers frequently underestimate the cost of foreign healthcare. In many regions, particularly the United States or remote island destinations, a single hospital stay or a specialized medical flight can exceed $100,000. Comprehensive policies typically offer limits starting at $250,000, with many experts recommending $1 million or more for high-cost destinations.

Navigating Political Unrest and Acts of War

A critical gap in many standard insurance policies involves the distinction between "acts of war" and "civil unrest." Recent global events, including the 2023 attempted coup and subsequent riots in Peru, have highlighted the limitations of basic coverage. Many travelers discovered that while their policies covered declared wars or terror attacks, they did not cover cancellations due to civil disturbances or political protests.

To address these "volatile region" risks, the insurance industry has popularized "Cancel for Any Reason" (CFAR) and "Interruption for Any Reason" (IFAR) riders.

Cancel for Any Reason (CFAR)

CFAR coverage allows a traveler to back out of a trip for any reason—including fear of travel due to rising political tensions—provided the cancellation occurs within a specific window (usually 48 to 72 hours) before departure. This coverage is typically more expensive and may only reimburse 50% to 75% of the non-refundable trip costs, but it provides a level of autonomy that standard policies lack.

Interruption for Any Reason (IFAR)

While CFAR applies before departure, IFAR is designed for situations that arise while the traveler is already at their destination. If a political situation deteriorates or a personal emergency requires a return home for someone not covered under the "immediate family" definition of a standard policy, IFAR allows the traveler to recover a portion of their unused expenses.

Regulatory Standards for Airline Delays and Cancellations

The logistical landscape of travel is heavily influenced by government regulations, which vary significantly by jurisdiction. Solo travelers must understand the protections afforded to them by the regions they are visiting or departing from.

United States: USDOT Regulations

The U.S. Department of Transportation (USDOT) recently updated its oversight, focusing on transparency through the Airline Cancellation and Delay Dashboard. While the USDOT has pushed for more consistent refunds, airlines are generally required to provide cash compensation only under specific circumstances. For most delays, the level of care (meals, hotels) is determined by the individual airline’s committed customer service plan.

Canada: The Canadian Transportation Agency (CTA)

Canada’s Air Passenger Protection Regulations distinguish between delays within an airline’s control and those outside of it (such as weather). Safety-related issues are considered "within the airline’s control," triggering requirements for compensation, assistance, and rebooking. If a delay is outside the airline’s control, the carrier is still mandated to ensure the passenger completes their journey, though financial compensation for inconvenience is not required.

The Timeline of Coverage: Why Timing Matters

One of the most common pitfalls for solo travelers is the delayed purchase of insurance. The "effective date" of a policy is crucial for several reasons:

- Pre-existing Conditions: To secure a waiver for pre-existing medical conditions, most insurers require the policy to be purchased within 10 to 21 days of the initial trip deposit.

- Known Events: Once a storm is named or a conflict is officially declared, it becomes a "known event." Travelers cannot purchase insurance after the fact to cover disruptions caused by that specific event.

- Stability Clauses: Many policies include a "stability period" (ranging from 60 days to 6 months). If a traveler’s medication changes or a condition flares up during this window before the trip, it may be excluded from coverage unless a pre-existing condition waiver was secured early.

Strategic Comparison: Single-Trip vs. Annual Policies

For the frequent solo traveler, the choice between single-trip and annual (multi-trip) insurance is a matter of both economics and convenience.

- Single-Trip Plans: These are tailored to a specific itinerary. They are often more comprehensive regarding trip cancellation and interruption values, making them ideal for high-cost, "once-in-a-lifetime" journeys.

- Annual Plans: These cover all trips taken within a 365-day period. They are generally more cost-effective for those traveling three or more times a year. However, annual plans often have a cap on the duration of any single trip (e.g., 30 or 60 days) and may offer lower limits for trip cancellation compared to single-trip policies.

The Role of Credit Cards and Secondary Insurance

Many travelers rely on the insurance benefits provided by premium credit cards. While these offer a valuable baseline of protection, they often contain significant gaps. Credit card coverage may have lower financial caps on medical expenses, may not cover emergency medical evacuation, and often excludes "adventure" activities or certain geographical regions.

Experts recommend a "gap analysis": comparing the credit card’s Summary of Benefits against a dedicated travel insurance policy. In many cases, a "top-up" policy is necessary to ensure full protection, particularly for medical emergencies and high-value trip non-refundables.

Industry Expert Perspectives and Analysis

The travel insurance market has seen a significant shift in consumer behavior following the 2020 pandemic. Data suggests a 30% increase in the attachment rate of insurance to travel bookings. Stan Sandberg, a co-founder of TravelInsurance.com, notes that natural disasters, such as volcanic eruptions or hurricanes, are covered under "mandatory evacuation" clauses, provided the policy was in place before the event became public knowledge.

Market analysts suggest that the rise of solo travel—particularly among the "silver traveler" (senior) demographic—is driving insurers to offer more nuanced products. Seniors, for instance, face higher premiums but require more robust coverage for pre-existing conditions and medical stability.

Broader Implications for the Global Traveler

The necessity of travel insurance reflects a world where travel is increasingly accessible but also more prone to systemic shocks. For the solo traveler, an insurance policy is more than a financial safety net; it is a portable support system. It provides access to 24/7 emergency hotlines that can coordinate with local hospitals, arrange for translation services, and manage the complex logistics of repatriation.

In conclusion, the modern solo traveler must view insurance as a non-negotiable fixed cost of exploration. By understanding the nuances of CFAR/IFAR policies, the importance of purchase timing, and the specific regulatory protections of their destination, travelers can ensure that their focus remains on the journey rather than the potential fallout of the unexpected. As global conditions continue to shift, the informed traveler remains the protected traveler.

{kind=link}