The Comprehensive Guide to Credit Card Transfer Partners and the Strategic Value of Flexible Rewards Ecosystems

The landscape of modern travel finance has undergone a fundamental shift, moving away from brand-specific loyalty and toward bank-issued transferable points. Financial institutions like American Express, Chase, and Capital One have established proprietary rewards currencies that offer significantly more utility than any single airline’s frequent flyer miles or hotel’s loyalty points. This value proposition is rooted in a single mechanism: the ability to move points to a diverse array of external travel partners. By leveraging these transfer ecosystems, savvy consumers can often double or triple the baseline value of their rewards, particularly when booking premium cabin international travel or high-end luxury hotel stays.

The Strategic Shift in Consumer Loyalty

Historically, travel loyalty was a binary choice: a consumer either earned miles with a specific airline or points with a specific hotel chain. However, the introduction of programs like Chase Ultimate Rewards and Amex Membership Rewards revolutionized the industry by creating a "currency of currencies." Today, the flexibility of these points acts as a hedge against the inevitable devaluations of individual airline programs. When one airline increases the number of miles required for a flight, a traveler with transferable points can simply pivot to a different partner within the same bank’s ecosystem.

The core principle of these programs is the transfer ratio, which is typically 1:1. This means that 100,000 bank points can become 100,000 airline miles. However, the process is a "one-way street." Once points are moved from a bank to an airline or hotel partner, they cannot be returned to the bank account. This necessitates a strategic approach where transfers are only initiated after confirming award availability for a specific itinerary.

Chase Ultimate Rewards: The Gold Standard for Beginners and Experts

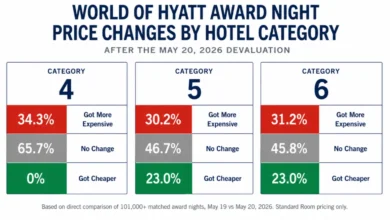

Chase has maintained a dominant position in the travel rewards sector through its Sapphire brand of credit cards. The ecosystem is anchored by the Chase Sapphire Preferred and the premium Chase Sapphire Reserve. Analysts frequently cite Chase’s partnership with the World of Hyatt as the program’s most significant competitive advantage. While many hotel programs have moved to dynamic pricing, Hyatt maintains a relatively stable award chart, often allowing points to be redeemed for 2 to 4 cents each—well above the industry average of 1 cent.

The Chase transfer portfolio includes approximately 14 partners, including major domestic carriers like United Airlines and Southwest, and international powerhouses like Singapore Airlines and British Airways. For travelers, the "Chase Trifecta"—a combination of a Sapphire card, a Freedom Flex, and a Freedom Unlimited—allows for accelerated point accumulation across all spending categories, which can then be pooled and transferred to high-value partners.

American Express Membership Rewards: The Original Powerhouse

American Express Membership Rewards is the oldest and most extensive transferable points program, currently boasting 20 airline and hotel partners. Amex distinguishes itself through the sheer volume of "transfer bonuses." These periodic promotions, which can range from 20% to 50%, allow cardmembers to receive more miles than the points they transfer. For example, a 40% bonus to Virgin Atlantic could turn 50,000 Amex points into 70,000 Virgin Atlantic Flying Club miles.

However, the Amex ecosystem includes unique friction points. Unlike its competitors, American Express is required by federal regulations to pass on an excise tax offset fee for transfers to U.S.-based airlines, such as Delta Air Lines and JetBlue. This fee is calculated at $0.0006 per point, capped at $99. Furthermore, while most transfers are 1:1, some partners like JetBlue and Hilton Honors utilize different ratios, requiring closer mathematical scrutiny from the consumer.

Capital One and Citi: The Mid-Market Disruptors

In recent years, Capital One has transitioned from a "fixed-value" rewards provider to a major player in the transferable points space. With the launch of the Venture X Rewards Credit Card in 2021, Capital One signaled its intent to compete directly with Chase and Amex. The program offers nearly 20 partners, with a heavy emphasis on international airlines like Air France-KLM (Flying Blue), Turkish Airlines, and British Airways. Most transfers are now 1:1, a significant improvement from the program’s earlier tiered ratio system.

Citi, through its ThankYou Rewards program, offers a more specialized list of partners. While it lacks a major domestic airline partner like United or Delta, it provides access to unique "sweet spots" via Turkish Airlines and Qatar Airways. One of Citi’s standout features is the ability to share points with any other ThankYou Rewards member, regardless of their relationship or address, though these shared points come with a strict 90-day expiration window.

Bilt Rewards: Revolutionizing the Rental Market

Bilt Rewards represents the most significant innovation in the loyalty space in the last decade. Launched with the premise of allowing renters to earn points on their monthly housing payments without transaction fees, Bilt has quickly assembled what many experts consider the highest-quality transfer portfolio in the industry. Bilt is currently the only major transferable currency that partners with both American Airlines and Alaska Airlines, in addition to high-value partners like World of Hyatt and United Airlines.

The program’s growth reflects a broader trend toward "lifestyle loyalty," where points are earned through everyday necessities—rent, dining, and local transit—rather than just travel spending. Bilt’s "Rent Day" promotions, occurring on the first of every month, often include massive transfer bonuses that exceed those offered by traditional banks.

Wells Fargo and Rove: The New Frontier

The newest entrants to the market, Wells Fargo and Rove, indicate that the appetite for transferable rewards is still growing. Wells Fargo recently revamped its Autograph card lineup to include transfer capabilities, focusing on a curated list of partners like Choice Privileges and British Airways. While the list is currently smaller than its peers, the bank has confirmed plans for future expansion.

Rove, a non-bank platform, offers a different model. It allows users to earn transferable points by booking through its travel portal or using its shopping extension. Rove’s unique selling proposition is the "instant credit" of miles upon booking nonrefundable hotel stays, providing immediate liquidity that traditional credit card billing cycles cannot match. This model appeals to a demographic that may not want to manage multiple high-annual-fee credit cards but still desires access to airline transfer "sweet spots."

Marriott Bonvoy: The Hotel Exception

While most hotel points are best used for hotel stays, Marriott Bonvoy points serve as a secondary transferable currency. Marriott maintains partnerships with nearly 40 airlines, many of which do not partner with any major bank. The standard transfer ratio is a less favorable 3:1. However, Marriott incentivizes large transfers by adding a 5,000-mile bonus for every 60,000 points moved to an airline (with some exceptions like American and Delta). For United Airlines specifically, the bonus is 10,000 miles, creating a more lucrative pathway for those with large balances of hotel points.

Chronology of the Transferable Points Evolution

The trajectory of these programs shows a clear move toward democratization. In the early 2000s, transferable points were largely reserved for high-net-worth individuals with Amex Centurion or Platinum cards. The 2009 launch of the Chase Sapphire Preferred brought this capability to the mass affluent market. By 2018, Capital One’s entry forced a standardization of 1:1 transfer ratios across the board. The 2021-2024 period has been defined by the entry of niche players like Bilt and the expansion of "no-annual-fee" cards that still offer transfer capabilities, such as the Wells Fargo Autograph and Citi Double Cash.

Data-Driven Analysis of Transfer Value

Financial analysts track the "cents per point" (CPP) value of these currencies to determine their relative worth. While a standard cashback card offers a fixed 1.0 CPP, transferable points are frequently valued between 1.7 and 2.2 CPP. This "premium" is attributed to the potential for high-value redemptions. For instance, a business-class seat to Europe might cost $4,000 or 60,000 miles. At 60,000 miles, the value realized is 6.6 CPP—more than six times the value of a standard cashback redemption.

Industry Implications and Future Outlook

The proliferation of transfer partners has led to increased competition among airlines to be included in bank ecosystems. For airlines, these partnerships represent a significant revenue stream, as banks purchase miles in bulk to distribute to cardholders. However, for consumers, the increased volume of points in circulation has led to "award inflation," where airlines occasionally increase the number of miles required for a seat without notice.

As the market matures, the distinction between a "traveler" and a "points strategist" is becoming clearer. The complexity of managing eight different programs and over 50 airline partners requires significant engagement. Nevertheless, the fundamental advantage remains: in an era of volatile travel pricing and devaluing loyalty programs, the flexibility provided by credit card transfer partners is the most effective tool for maintaining the purchasing power of one’s rewards. Experts predict that the next phase of this evolution will involve more integrated search tools and AI-driven recommendations to help consumers navigate the increasingly complex web of transfer options.

{kind=link}